Executive Summary

Executive Summary

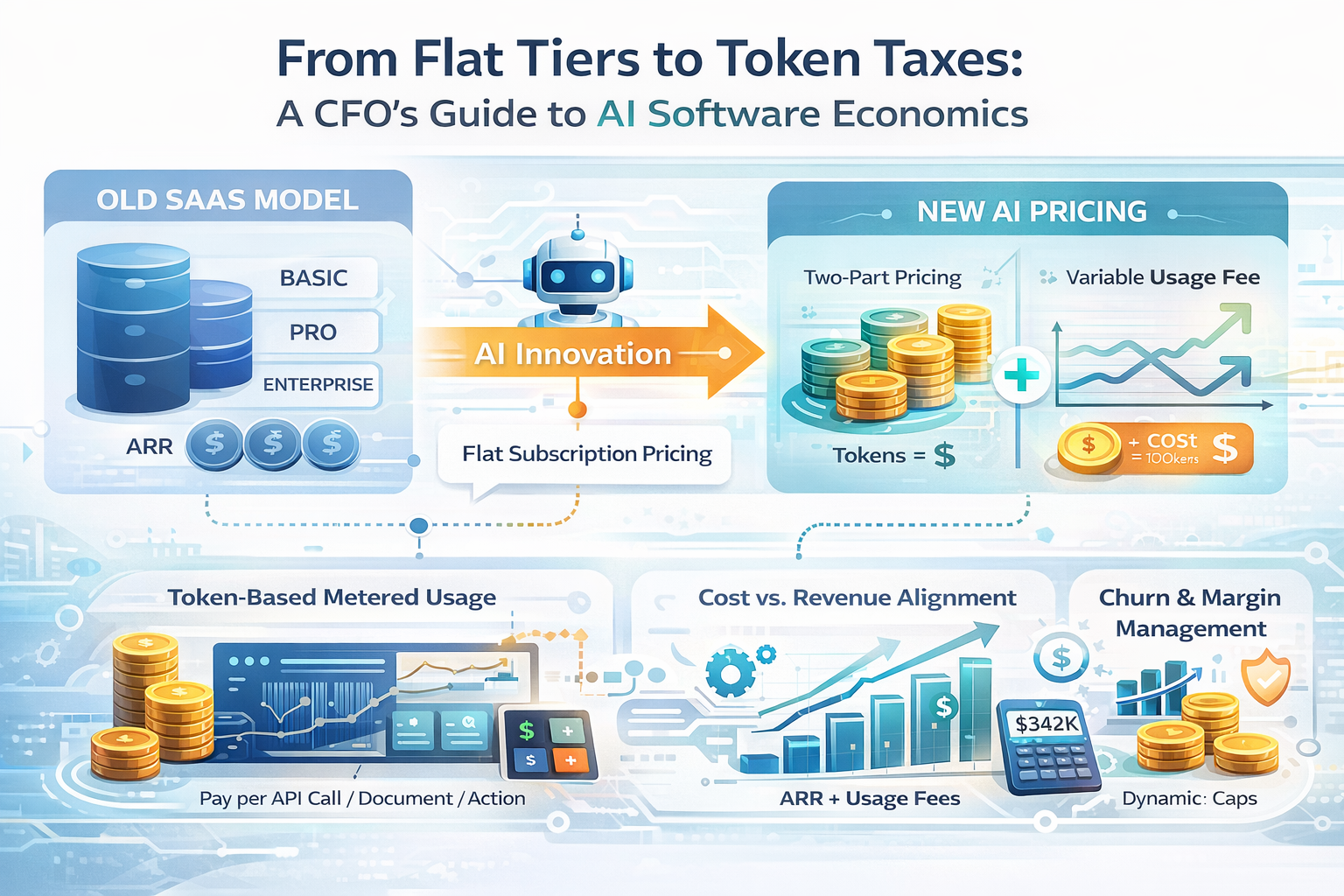

AI is forcing the third major rethink of the software pricing model, after perpetual/site licensing approach gave way to SaaS subscriptions. For software CFOs, the core shifts are:

Pricing moves from flat tiers to two-part models (fixed subscription + variable usage based pricing). This eliminates the hidden cross-subsidy inherent in SaaS pricing where light users subsidized heavy users. Newer approach lets revenue scale with value delivered, and captures consumer surplus that rigid SaaS tiers left on the table. But it introduces revenue volatility, customer pushback for fixed-price contracts, and a working-capital mismatch between upfront cash collection and uneven compute costs.

COGS returns to software. Inference costs reintroduce meaningful marginal cost, compressing gross margins from 80%+ to 50–70% levels. Unlike traditional SaaS where margin was a result, AI gross margin is a managed output shaped by model routing, caching, and diversification. Two startups with identical products can have radically different margins depending on how they manage inference.

Every core SaaS metric needs reinterpretation. ARR becomes a floor, not the full picture. NRR must be decomposed into subscription retention and usage expansion. Revenue quality (durable vs. volatile) matters as much as revenue growth. LTV becomes a function of usage intensity and cost-to-serve. CAC payback extends. A/B testing becomes a contribution margin decision, not just an engagement one.

Adjacent functions get a rethink. Support tiers lose their value proposition as AI accelerate bug detection, triage and resolution times. Therefore premiums shift to accountability and outcome based pricing. Customer success evolves from maximizing usage to managing “profitable” usage. R&D capitalization needs to distinguish durable platform assets from application-layer code with shorter useful lives.

The startup cost advantage is real but temporary. Now startups can undercut incumbents on price because their development economics are fundamentally different with little or no legacy costs. However, this window closes as incumbents adopt the same AI tools and paradigms. For successful business, startup founders should be aware that other costs (distribution, trust, inertia) and complexities remain the same.

Introduction

Software pricing has reinvented itself before. Perpetual and site licenses gave way to SaaS subscriptions, and an entire financial vocabulary followed: ARR, MRR, NRR, CAC, LTV, payback period etc. CFOs learned a new language, investors built new valuation frameworks around it, and this transition took a decade to play out. AI is forcing the next one, and this time the shift is more complex and disruptive. As AI-assisted development drives the cost of developing software toward zero, every layer of the software business model moves: how you price, what you account for, where margin lives, and what metrics you should measure!

From Rigid Tiers to Continuous Pricing

SaaS pricing was always blunt tool. Freemium to generate leads, a mid-tier for teams, enterprise tier for the bigger companies. Everyone in a tier paid the same regardless of value extracted or cost to serve. ARR was clean because you could multiply customers by plan price and track expansion through tier upgrades.

SaaS created a hidden cross-subsidy where light users effectively subsidized heavy users. When marginal cost was near zero, nobody noticed because the cost of serving a power user was barely different from serving a casual one. LTV calculations could safely assume uniform cost-to-serve across a cohort, and that assumption held for two decades.

AI destroys it. Heavy usage now carries real cost, and a power user running hundreds of inference calls a day is materially more expensive to serve than someone who logs in weekly. The cross-subsidy stops being invisible and starts destroying your margin: your most engaged customers, the ones with the highest potential LTV, become your most expensive to serve, while the flat tier price prevents you from recovering a dollar of it.

The two-part model that's emerging fixes this directly. A fixed subscription covers the baseline (access, reliability, platform), while a variable component meters AI consumption per query, per document, or per agent action. Cost and revenue scale together, the cross-subsidy disappears, and each customer's unit economics stand on their own.

For startup CFOs, this rewrites how you model the business:

- ARR becomes a floor, not the whole story. Total revenue is subscription plus usage, and the usage layer can grow without a single seat expansion or tier upgrade.

- NRR also gets a new driver. Usage expansion can push it over 100% without any new subscriptions.

- Forecasting gets harder. You now need cohort-level usage analysis rather than just retention and expansion rates, which introduces complexity most early-stage finance teams aren't built for.

The New Churn Dynamics

Discrete tiers in SaaS made retention binary: customers renewed or they didn't, and your customer success team either pushed them up a tier or kept them from leaving. Variable pricing makes churn continuous because there are no cliffs between tiers. If customers see their bill fluctuate, and every spike becomes a moment of doubt.

A $2,000 usage charge on top of a $500 subscription doesn't trigger a cancellation. It triggers a behavior change where customers quietly stop using the expensive features. MRR erodes without customer churn, and NRR can slip through usage contraction.

This creates an unavoidable tension: even though two-part pricing is economically efficient, but the reality is customers hate unpredictable bills. Enterprise procurement teams budget annually, and a cost line that swings quarter to quarter is not welcome. To mitigate this, many customers will demand fixed-price contracts that shift usage risk entirely to the software vendor.

Every startup CFO will face this negotiation, and the options carry tradeoffs:

- Say yes to fixed pricing and your gross margins are exposed if usage spikes. You are effectively underwriting the customer's consumption.

- Say no and you risk losing the deal to a competitor willing to absorb the risk.

- The middle ground is usage caps with overage rates, but getting the cap levels right requires usage data you may not have yet.

This tension will generate new infrastructure and new financial products:

- Usage-based billing systems with real-time metering, contract-specific rate cards, and threshold alerts become core operational capabilities rather than afterthoughts. This can reduce billing friction with the customer.

- Insurance and hedging products may emerge for either side. Customers pay a premium to cap monthly AI costs; vendors hedge the margin exposure of fixed-price contracts. This mirrors how energy markets evolved when electricity moved from flat rates to spot pricing and an entire ecosystem of hedging instruments followed.

A/B Testing Becomes a Financial Decision

In traditional SaaS, A/B testing was purely a product question. You showed users two variants, measured engagement, and shipped the winner. Both variants cost the same to serve, so the only dimension that mattered was preference.

When features carry real inference cost, user preference alone is insufficient. A feature that wins on engagement but burns 5x the compute of the alternative destroys value at scale, which means the right question stops being "which do users prefer?" and becomes "which generates more contribution margin?"

Consider two versions of an AI recommendation engine:

- Version A uses a large, expensive model and produces slightly better suggestions. It wins the satisfaction survey.

- Version B uses a smaller model and produces results that are almost as good. It generates 40% more contribution margin per user per month.

Across your customer base, that difference compounds into a material P&L impact that no product review would surface on its own. Product and finance now have to collaborate on experimentation in ways they never did before:

- Every A/B test needs a cost dimension alongside the engagement dimension.

- The product team needs real-time visibility into inference cost per variant.

- The finance team needs to define contribution margin thresholds for shipping expensive features.

- Some features will justify the higher cost because they drive retention or unlock usage revenue. Others will look great in a demo and quietly erode gross margin at scale.

For startup CFOs, this is a new muscle. You need instrumentation that ties feature-level usage to feature-level cost, a framework for evaluating experiments on contribution margin rather than conversion alone, and the willingness to kill features that users like but the business can't afford. When marginal cost was zero, product had the final word on what shipped. When there's real COGS, the CFO earns a seat at that table.

Support Tiers Get A Rethink

SaaS companies have long sold tiered support as a revenue lever, with basic plans offering email support at 48-hour response times, premium plans adding dedicated managers and priority bug fixes, and enterprise plans layering on SLAs and custom integrations. The pricing gap between tiers often had more to do with support commitments than product functionality.

This model rested on a constraint: the development pipeline was slow. Bugs entered a backlog and shipped weeks later, and premium support didn't mean the fix arrived faster in absolute terms. It meant your bug got prioritized higher in a queue that moved at a slower pace. **Customers were paying for position in line, not for a fundamentally different speed of resolution. ** Imagine a world where resolution is much less expensive in terms of cost and time. With AI-assisted development, both these change:

- Detection: AI-powered monitoring identifies bugs and regressions before customers report them. The support ticket infrastructure that used to start the process slowly becomes redundant for a growing class of issues.

- Resolution: AI-assisted coding compresses fix times from weeks to hours for well-scoped problems. The backlog clears faster than it fills. So, the value of resolution by support tier erodes.

If fast detection and resolution becomes the default, the support premium has to be redefined around things AI can't replicate: dedicated relationship management, proactive architecture reviews, contractual SLAs with financial penalties. The value shifts from ticket velocity to accountability and strategic partnership.

For startup CFOs, this hits the P&L directly. Support tiering was high-margin revenue because the cost difference between tiers was mostly labor allocation. If AI compresses support costs, you face a choice: premium margins shrink because you have to deliver genuinely differentiated service, or lower-tier pricing rises because the baseline is now much better. Either way, the support revenue model needs to be rethought around what remains scarce: human judgment, relationship continuity, and contractual risk absorption.

COGS (Cost of Goods Sold) Returns to Software

Everything in this article traces back to one structural change that token cost create: AI reintroduces cost of goods sold (COGs) for software companies. Traditional SaaS had near-zero marginal cost, with gross margins of 80 to 90% so standard that investors used 70% as a minimum threshold.

AI changes the math fundamentally. **Every inference call burns compute, and the "token cost" scales with usage in a way SaaS never experienced. **So, AI-native products will operate at lower gross margin of 50 to 70%. This shift alone has several cascading effects:

- LTV compresses because cost-to-serve rises while revenue per customer may not.

- CAC payback extends unless pricing compensates for the margin compression.

- Investor expectations shift. The 80%+ gross margin that once qualified you for premium multiples may no longer be achievable, and your narrative has to explain why at 60%, you have a great business.

COGS becomes a strategic line item that demands active management. Track inference cost per customer, per feature, and per use case. Build inference routing (cheap models for simple queries, expensive ones for complex work for example) as a margin discipline rather than just an engineering choice. Software CFO's job now includes understanding model economics the way a manufacturing CFO understands raw materials and value chain.

On thing to note here is that two-part pricing mechanism makes the AI software pricing sustainable. The variable component passes inference cost through to the customer, keeping the LTV/CAC ratio healthy even for power users, while the fixed component provides stability.

R&D Capitalization Needs Rethinking

Under ASC 350-40 and IAS 38 accounting standards, software companies can capitalize software development costs at technological feasibility and amortize it over three to five years. This made sense when code was expensive to develop and durable once written, but both assumptions are weakening with AI.

- Less to capitalize. Development costs drop substantially when AI tools do much of the work.

- Shorter useful life. Application software depreciates faster when a competitor can regenerate comparable functionality in a short time.

Capitalizing inflates the balance sheet and smooths the income statement, but if the asset depreciates faster than your amortization schedule, you're building in a future write-down. Therefore, most likely, the answer may be to expense application software development in the future. Platform infrastructure and proprietary data pipelines still have multi-year useful lives, but application-layer code (features, UI, business logic) may not. Accounting has to match the economic reality rather than the other way around - this will require a rethink by accountants and a better understanding of what the product features.

The Cost Gap Creates a Window

Incumbents spent years and hundreds of millions building their platforms, and their pricing approach reflects that accumulated investment. A startup building with AI reaches comparable functionality with a fraction of the cost and time. This allows startups to price their offering at a fraction of what incumbent's can, while still running healthy unit economics.

This is the same dynamic that played out in the licensing-to-SaaS transition, where incumbents anchored to large upfront deals couldn't shift to subscriptions without a revenue hit, and Salesforce used that opening to capture market share. AI creates a similar window: incumbents who are anchored to pricing that reflects legacy cost structures, and startups can undercut them because their unit economics are different.

The window isn't permanent, because incumbents will adopt the same AI tools and compress their own costs over time.

Building the Financial Architecture

If you're building a startup's financial model today, here's the checklist:

- Price as a two-part structure from day one so each customer's unit economics are self-sustaining.

- Build billing infrastructure early. Metering, rate cards, and usage alerts are must-haves when your pricing depends on them.

- Prepare for fixed-price negotiations by understanding usage distributions well enough to set caps to protect margin.

- Integrate contribution margin into A/B testing so product decisions reflect their true cost at scale.

- Rebuild support revenue around accountability rather than queue position.

- Manage COGS like a supply chain. Track inference cost per customer, per feature, per use case.

- Revisit R&D capitalization in light of lower development costs and shorter useful lives.

- Decompose NRR into subscription retention and usage expansion so your board sees what's actually driving the number.

Margins for software companies will settle lower, ARR becomes a floor, NRR gets harder to predict and achieve, and product decisions carry financial weight they never had before. New financial products will emerge to manage the billing complexity and volatility that replaces the old predictability. But software will remain one of the best businesses in the world. It's just learning a new financial language and new tricks, the same way it did when licensing approach gave way to SaaS subscription.

Navigating AI economics requires the kind of forward-looking financial leadership that a fractional CFO provides. StartupCFO works with AI-native founders to build financial models that account for inference COGS, usage-based revenue, and R&D capitalization strategy, with ClariFi tracking the unit economics that matter most. See our startup CFO services or talk to our team.